The Partnership sends updates for the most important economic indicators each month. If you would like to opt-in to receive these updates, please click here.

Estimated Read Time: 1 minute

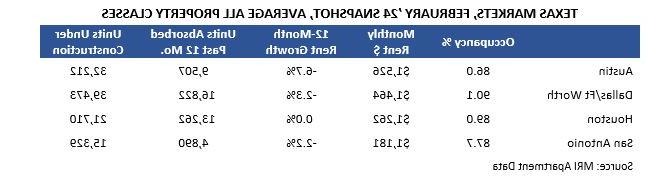

Developers continue to deliver more apartment units to the market than Houston can absorb, pushing down occupancy rates and monthly rents. Landlords have turned to incentives to entice renters to sign leases. Houston is not alone. Austin, Dallas/Fort Worth, and San Antonio are in similar situations.

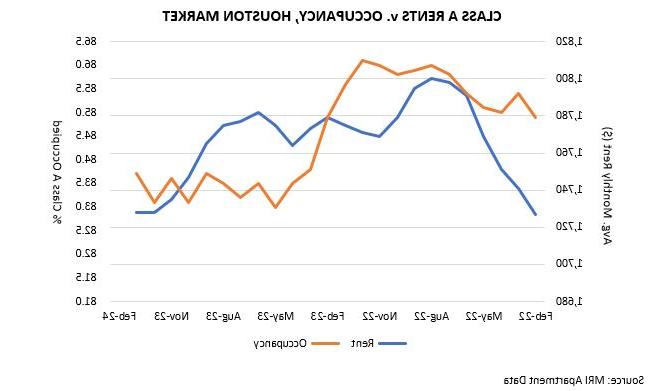

Local developers have delivered over 35,500 Class A units (i.e., the newest apartments with high levels of amenities) since February ’22. The market has absorbed only 28,700 of those units. Overall occupancy has dropped 1.2 percentage points over the period and rents have remained flat.

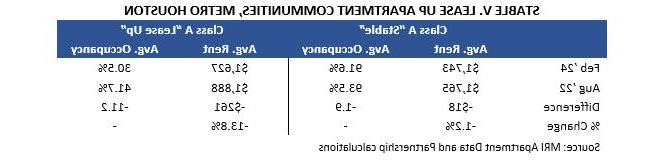

Occupancy and rents for “stable” properties (i.e., open more than 13 months) have held up well while those in “lease up” (i.e., open less than 13 months) have struggled to attract tenants and maintain rents.

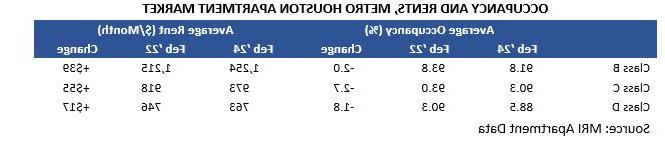

Class B, C and D properties have struggled as well, logging negative absorption over the last two years. Combined, the group has shed over 7,000 tenants since February ’22.

Rents have held up better than expected, however, increasing marginally over the period. But the increases have not kept up with inflation and landlords’ higher operating costs.

Class D occupancy has dropped below 90 percent and Class C is sliding toward that level. That’s a critical threshold. Rates above 90 percent reflect a landlord-friendly market, below 90 percent a tenant-friendly market. As the market continues to soften, landlords may soon see their recent rent gains evaporate.

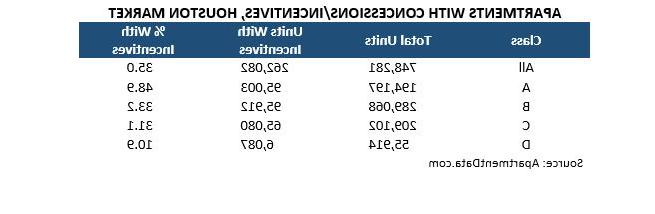

The decline in occupancy has spurred owners to offer incentives or concessions to draw prospective tenants to their properties. This may include free rent, waiver of a security deposit, or floorplan upgrades. As of February ’24, incentives were available on over one-third of all apartment units in Houston. Nearly half of all Class A units have an incentive.

Houston is performing marginally better than other Texas metros, with Austin, Dallas/Fort Worth, and San Antonio experiencing greater declines in rental growth over the past 12 months.

In Austin, incentives are available on 44 percent of all apartments, in Dallas/Fort Worth on 36 percent, and in San Antonio on 43 percent.

As of February ’24, there were 21,710 apartment units under construction in Houston of which 70 percent will deliver this year. Another 33,863 are proposed.

Prepared by Greater Houston Partnership Research Department

Patrick Jankowski, CERP

Chief Economist

Senior Vice President, Research

pjankowski@joyerianicaragua.com

Leta Wauson

Research Director

713-844-3661

lwauson@joyerianicaragua.com

The occupancy rate for Class A units in Jan '24

View data on the cost of living in Houston compared with other major U.S. metros.

Review the latest data on this key economic indicator.

Review the latest information on home sales in the Houston region.

Stay up-to-date on what’s happening with the Partnership and Greater Houston region by opting-in to receive information on upcoming events, news, data releases and more.